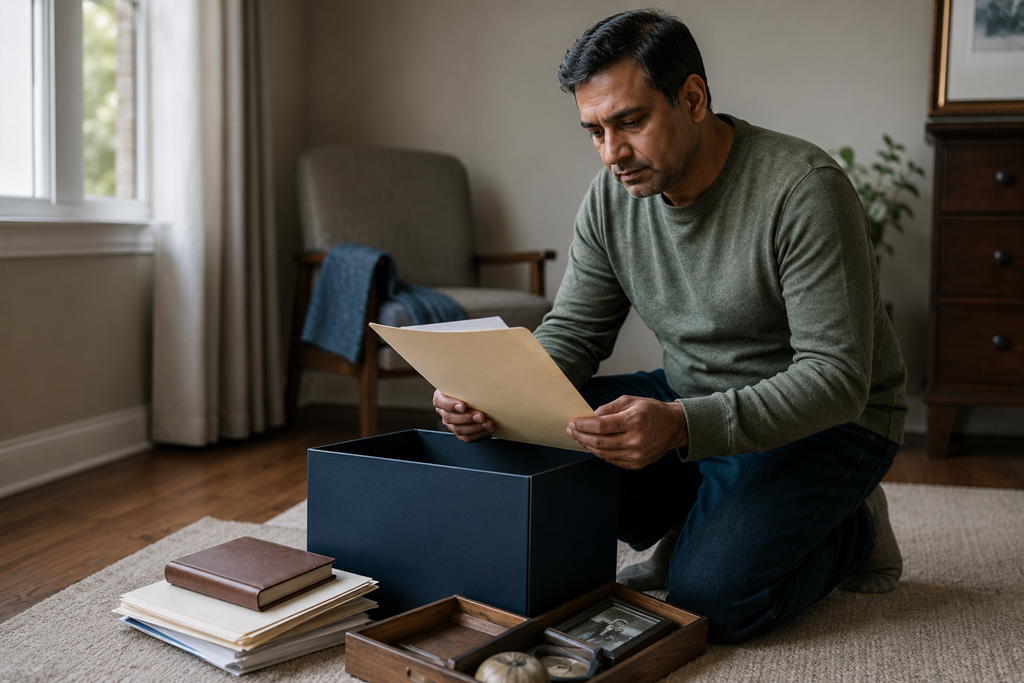

Many people avoid looking at their retirement accounts because the account does not feel like a simple number on a screen or statement. It can feel like a judgment, a reminder, a question, or a measurement of whether they are “on track” in life.

That is why the avoidance often has less to do with laziness and more to do with discomfort.

A person may know they should check their balance, review contributions, or understand what is happening with their retirement money. But when the account feels tied to fear, regret, confusion, or comparison, even opening it can feel heavier than expected.

The simple answer is this: many people avoid looking at their retirement accounts because they are not just avoiding information. They are avoiding the emotions they expect the information to bring up.

The Account Can Start To Feel Like A Verdict

A retirement account is supposed to be a tool. But for many people, it starts to feel like a verdict on past choices.

Someone may open their account and immediately think about years they did not contribute, jobs that did not offer strong benefits, financial setbacks, medical bills, family responsibilities, debt, or periods when saving simply was not realistic.

The balance becomes more than a balance.

It can feel like proof that they are behind, even when they do not know what “behind” actually means for their age, income, household, goals, or lifestyle. That emotional jump can make the account feel unsafe to look at, even if the numbers themselves are only information.

This is one reason avoidance can be so easy to misunderstand. From the outside, it may look like someone does not care about retirement. In reality, they may care so much that the account feels difficult to face.

Not Knowing What The Numbers Mean Makes It Harder

Retirement accounts can be confusing because the balance alone does not explain everything.

A person may see a number and wonder:

Is this enough?

Am I contributing enough?

Should the balance be higher?

Did I choose the wrong investments?

Why did the account go down?

What does this actually mean for my future?

Without context, the account can create more questions than answers. That uncertainty often leads people to shut the statement, close the app, or tell themselves they will look later.

The problem is not always the number. Sometimes the problem is that the number arrives without translation.

Retirement accounts often use financial terms that feel distant from everyday life. Contribution rates, asset allocation, vesting schedules, expense ratios, employer matches, rollovers, and market performance can make a person feel as if they are supposed to understand a system they were never taught.

When people feel unprepared to interpret what they see, avoiding the account can feel easier than staring at information that makes them feel behind or out of place.

Shame Can Make A Normal Check-In Feel Personal

One of the strongest reasons people avoid retirement accounts is shame.

Shame can show up quietly. It may sound like:

I should have started earlier.

I should have saved more.

I should understand this by now.

Other people probably have more than I do.

I waited too long.

These thoughts can make a routine account review feel personal. Instead of seeing the account as a financial tool, the person starts seeing it as evidence of failure.

But retirement saving does not happen in a vacuum. People deal with rent or mortgage payments, child care, job changes, caregiving, inflation, medical expenses, student loans, emergencies, and income limits. Many people are trying to make good choices inside real constraints.

That does not mean retirement planning should be ignored. It means the account balance should not be treated as the full story of a person’s effort, discipline, or worth.

Some People Avoid The Account Because They Fear Bad News

Avoidance often grows when someone expects the account to disappoint them.

They may assume the balance is too low. They may worry the market dropped. They may fear they forgot to update something important. They may wonder whether an old employer account is sitting untouched somewhere. They may suspect they are not contributing enough but do not want to confirm it.

This creates a strange emotional trap.

The person does not look because they are afraid the information will feel bad. But not looking can make the unknown feel even bigger.

The account becomes a closed door. Behind that door, the mind can imagine the worst. Sometimes the imagined version feels more intimidating than the real information would be.

That is why avoidance can increase anxiety instead of reducing it. It may offer short-term relief, but the uncertainty remains.

Looking Does Not Mean You Have To Fix Everything Immediately

A common misunderstanding is that checking a retirement account means a person must immediately make big decisions.

That belief can make the task feel too large.

Someone may think that if they look, they will need to change investments, increase contributions, call a financial professional, understand every fund option, calculate a retirement number, and rebuild their entire plan.

But looking at the account does not have to mean solving everything at once.

Sometimes looking simply means becoming familiar with what is there. It can mean noticing the balance, seeing whether contributions are happening, confirming the account is active, or understanding where the money is held.

That kind of awareness matters because it separates information from panic. A person can observe the account without turning the moment into a full financial overhaul.

The first look does not have to carry the weight of every future decision.

Avoidance Can Be A Sign That The Topic Needs More Support

Avoiding a retirement account is not always a character flaw. Often, it is a signal.

It may signal that the person needs simpler explanations. It may signal that retirement feels too abstract. It may signal that money has been stressful for a long time. It may signal that the person has never had a trusted space to ask basic questions without feeling judged.

Many people were never taught how retirement accounts work. They were simply handed enrollment forms, workplace benefits packets, online portals, or account statements and expected to make confident decisions.

That can leave people feeling embarrassed about not knowing things that are actually very common to misunderstand.

Avoidance often softens when the account becomes less mysterious. The more a person understands what they are looking at, the less the account feels like a threat and the more it becomes a source of useful information.

Comparing Your Account To Someone Else’s Can Make Avoidance Worse

Comparison can also make people avoid their retirement accounts.

They may hear coworkers talk about investing, see online conversations about retirement goals, or compare themselves to friends who seem more financially prepared. This can make their own account feel disappointing before they even open it.

But retirement accounts are shaped by many private details: income history, employer benefits, family responsibilities, cost of living, health needs, debt, age, job stability, and when someone first had access to retirement savings.

Two people can be the same age and still have very different financial paths.

Comparison can create a false sense of failure because it ignores context. A retirement account is most useful when it helps a person understand their own situation, not when it becomes a scoreboard against someone else’s life.

The Account Is Information, Not An Identity

One helpful reframe is to remember that a retirement account is information.

It is not a final grade.

It is not a full measure of responsibility.

It is not proof that a person has failed.

It is a snapshot of where one part of their financial life stands right now.

That snapshot may show progress. It may show gaps. It may show something that needs attention. But it is still information, and information is easier to work with than uncertainty.

Avoidance keeps the account emotionally large. Looking at it, even briefly, can make it more specific. Specific information is not always comfortable, but it is usually more workable than a vague fear.

A Better Relationship With The Account Starts With Less Judgment

Many people avoid looking at their retirement accounts because they expect the experience to make them feel worse. That expectation is understandable, especially if money has often been tied to stress, regret, or pressure.

But the account itself is not there to accuse anyone. It is there to show information that can help shape future choices.

The goal is not to feel perfect about the number. The goal is to reduce the mystery around it.

A retirement account becomes less intimidating when it is treated as a tool instead of a verdict. It may still bring up feelings, but those feelings do not have to control whether the account gets opened.

Looking does not mean everything is solved. It simply means the unknown has less room to grow.

Download Our Free E-book!