Financial planning fatigue often shows up before full shutdown as a quieter pattern of mental resistance. You may still care about your finances, but your energy for thinking about them starts to fade. Tasks you would normally handle begin to feel heavier than they should. You put off decisions, avoid reviewing accounts, feel unusually tense when money comes up, or notice that even small financial choices now seem harder to process.

This is not always obvious at first. It can look like procrastination, indecision, or a lack of motivation. But often the deeper issue is that your mind has been carrying too much financial responsibility, uncertainty, and ongoing evaluation for too long. The fatigue begins before complete disengagement. The key is noticing the change in how your financial life feels, not just whether you are still technically keeping up with it.

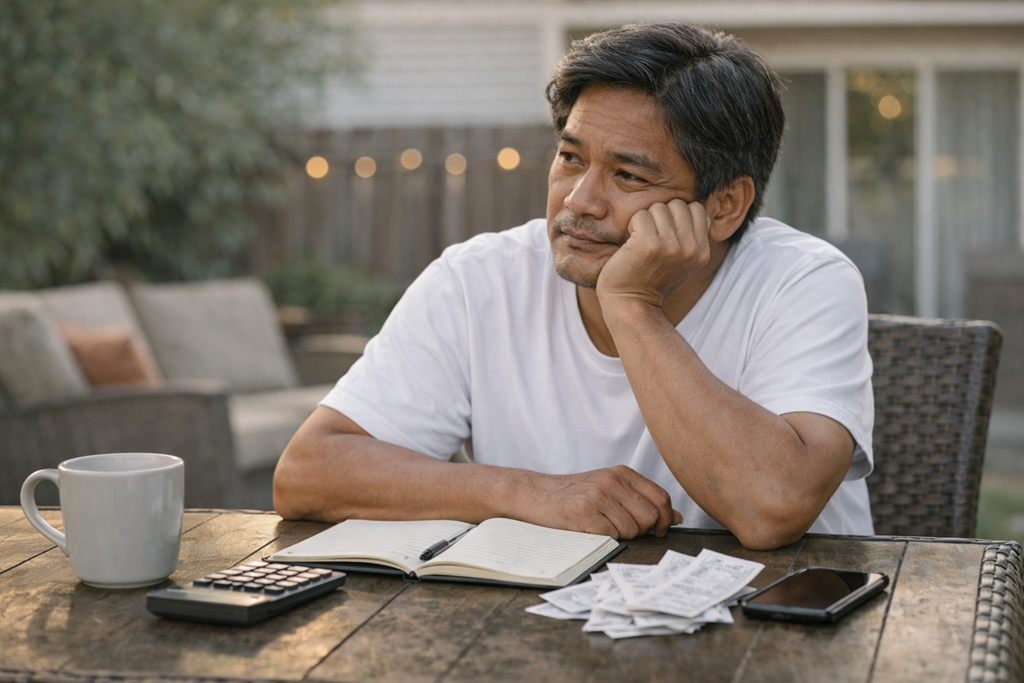

When responsible money habits start feeling strangely hard to touch

One of the earliest signs of financial planning fatigue is that ordinary money tasks begin to feel emotionally expensive.

Maybe you usually review your budget without much trouble, but now you keep postponing it. Maybe you mean to look at your retirement contributions, savings goals, or upcoming expenses, but you find yourself avoiding the topic altogether. Maybe you open a spreadsheet or banking app, then close it again because you do not have the energy to think through one more decision.

That shift matters.

Financial fatigue does not always begin with chaos. Sometimes it begins when familiar routines start producing more tension than clarity. The work may not even be objectively difficult. It just feels harder to access mentally.

This is often what people miss. They assume burnout only counts once they have fully checked out. In reality, fatigue usually shows itself earlier through reluctance, irritability, indecision, and a growing sense that money has become one more thing your brain does not want to hold.

The warning signs are often subtle before they become obvious

Before people shut down around money, they often pass through a stage where their financial life feels noisier, heavier, or harder to organize internally.

You might notice that small decisions are taking longer than usual. You might second-guess choices you would normally make with little trouble. You might feel a low-grade dread before checking balances, reviewing bills, or talking with a partner about money. You may even keep thinking about financial issues in the background without making much progress on them.

That combination is important: constant mental presence with reduced clarity.

A helpful way to recognize financial planning fatigue is to pay attention to friction. Not just whether you are doing the task, but how much inner drag the task now creates. When routine financial care begins requiring disproportionate mental effort, that is often a signal that your planning process is no longer fully supporting you.

Why recognizing it early makes such a difference

Catching financial planning fatigue early matters because untreated fatigue often turns into avoidance.

At first, the strain may only affect how a task feels. Later, it can begin affecting whether the task happens at all. A postponed account review becomes several postponed reviews. A decision you meant to revisit stays unresolved for weeks. Financial conversations become easier to defer. The more overloaded the mind feels, the more likely it is to seek distance from the topic entirely.

That can create a discouraging cycle. The person avoids money because they are tired, then feels worse because the avoidance creates more uncertainty. More uncertainty creates more pressure, which creates even more fatigue.

Recognizing the issue earlier interrupts that pattern with understanding instead of self-criticism.

One of the most clarifying insights here is that financial fatigue is not only about the amount of work involved. It is also about the amount of ongoing mental openness your finances require. Too many unresolved decisions, too much self-monitoring, and too many future-oriented questions can drain energy even when nothing has gone “wrong” on paper.

What to pay attention to when your financial life starts feeling heavier

Early recognition often comes from noticing patterns rather than waiting for a dramatic breaking point.

One pattern is emotional thinning. You feel less patient, less clear, or less resilient when money comes up. Another is repetitive deferral. You keep telling yourself you will think about it later, but later keeps moving. Another is overcomplication. Everything starts seeming important, interconnected, or too high-stakes to approach casually. Another is mental spillover. Financial decisions follow you into unrelated parts of the day, quietly occupying space even when you are not actively working on them.

None of these signs mean you are irresponsible. They usually mean your system is demanding more active mental energy than it should.

That is worth taking seriously, not in an alarmed way, but in an honest one. A sustainable financial life should not require constant inner bracing.

It is easy to misread the problem and push yourself in the wrong direction

A common misunderstanding is assuming that if money feels harder to deal with, the answer must be more discipline.

Sometimes what people actually need is less friction, not more pressure.

Another misunderstanding is treating fatigue as proof that you do not care enough about the future. In many cases, financial fatigue develops precisely because you do care. You are trying to think ahead, be responsible, avoid mistakes, and protect stability. The exhaustion comes from carrying that responsibility too continuously, not from failing to value it.

It is also easy to assume that burnout only applies when finances are in crisis. But planning fatigue can build inside relatively stable situations too. The issue is not only financial hardship. It is the ongoing cognitive load of managing choices, uncertainty, and long-term consequences.

This matters because people often respond to early fatigue by increasing research, increasing self-monitoring, or trying to “finally get fully on top of it.” Sometimes that deepens the strain. It keeps the person in a mode of constant evaluation when what they really need is a more sustainable relationship to planning.

Recognition should lead to gentleness, not shame

The most useful response to early financial fatigue is not self-judgment. It is a calmer kind of honesty.

If your financial life has started feeling unusually heavy, that does not automatically mean you are behind or failing. It may mean your mind is asking for a different pacing, a simpler structure, or fewer active decisions at once. That recognition can be deeply stabilizing because it replaces vague frustration with something more accurate.

You do not need to wait until you are fully shut down to take your own strain seriously. In fact, the earlier you notice the drag, the easier it becomes to protect clarity before avoidance takes over.

If this pattern feels familiar, the Hub article, Why Long-Term Financial Planning Can Become A Quiet Form Of Financial Burnout, explores the broader emotional and mental load behind this kind of exhaustion and why it can build even in people who are trying hard to do the right thing.

Financial burnout often begins as friction, not failure

Recognizing financial planning fatigue early means noticing when money starts feeling harder to hold than it used to.

That might look like avoidance, indecision, dread, repetitive overthinking, or simple mental weariness around tasks that used to feel manageable. These are not signs that you have become careless. They are often signs that your current planning rhythm is asking too much of your mental energy.

The good news is that awareness can come before shutdown. And once you can name what is happening more clearly, it becomes easier to respond with steadiness instead of shame.

Download Our Free E-book!