Supporting more than one generation at the same time can create a kind of financial stress that is hard to explain to people who have not lived it.

It is not just the pressure of paying bills. It is the pressure of trying to be responsible in several directions at once. You may be helping children with housing, food, school costs, childcare, or early adult expenses while also helping parents with medical costs, living expenses, transportation, housing support, or day-to-day gaps in their budget. In many families, this happens gradually. At first it looks temporary. Then it becomes a normal part of life.

What makes this kind of strain different is that the money pressure is rarely the only pressure. It is often tied to love, duty, identity, culture, loyalty, and fear of what might happen if you stop holding things together. Many people in this position are not acting carelessly. They are often the most dependable person in the family. They are trying to do the right thing. That is exactly why the stress can become so heavy.

This problem is more common than many people realize. Plenty of adults are trying to protect their own household while also acting as a stabilizer for relatives across generations. If that is your reality, it does not mean you are weak, bad with money, or failing at adulthood. It usually means you are carrying a financial role that is larger, more emotionally loaded, and more structurally complex than it first appears.

What This Financial Stress Really Looks Like in Real Life

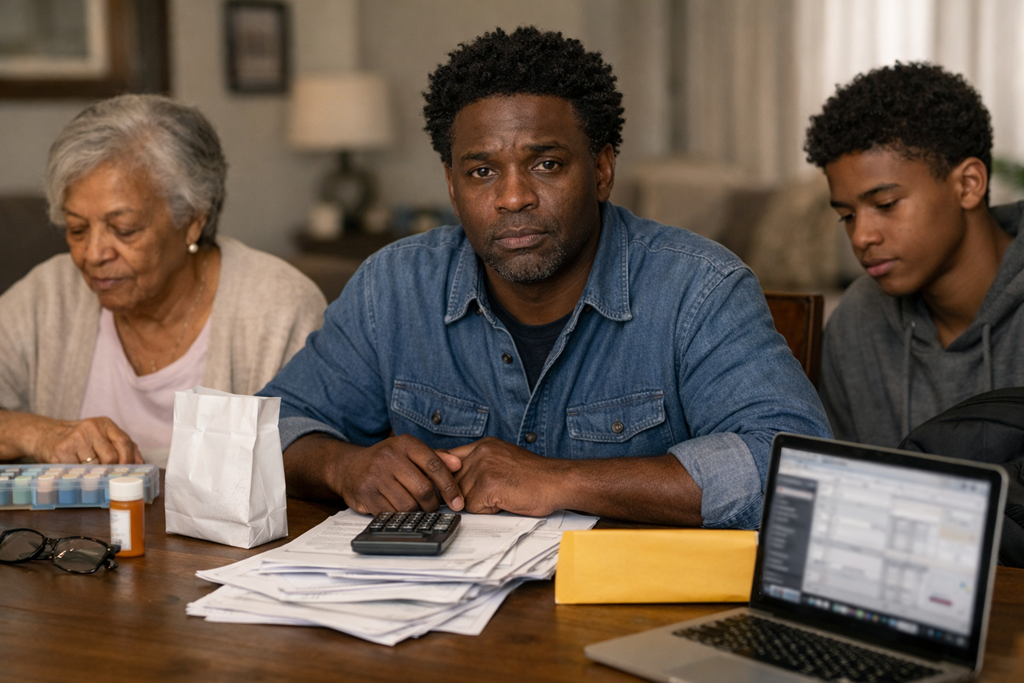

Multi-generational financial responsibility stress happens when one person or household feels responsible for the financial wellbeing of both older and younger family members at the same time.

In real life, this can look like:

paying your own mortgage or rent while helping a parent with prescriptions or utilities

covering child expenses while also helping an adult child through a rough season

trying to save for retirement while dealing with ongoing family emergencies

saying yes to one generation because the other generation already needs so much

feeling like every financial decision affects more people than just your own household

The emotional experience often includes constant mental load. Even when no crisis is happening, part of your brain may stay alert. You may be calculating, anticipating, delaying, adjusting, and quietly worrying. You may feel guilty when you spend on yourself. You may feel guilty when you say no. You may feel guilty even when you say yes, because you know it may hurt your own long-term stability.

That is part of what makes this stress so difficult. It is not always dramatic from the outside. Sometimes it looks like a capable adult who is managing everything. Inside, it can feel like there is never enough margin, never a fully safe answer, and never a clean line between generosity and overextension.

A lot of people assume financial stress should be simple to identify: either you can afford things or you cannot. But multi-generational pressure does not work that way. Someone can earn a decent income and still feel financially trapped because the number of people depending on that income keeps expanding. Someone can look stable on paper while feeling deeply stretched in practice.

This is also why the experience can feel isolating. Traditional financial advice often assumes a person is planning for one household with relatively clear priorities. But many people are managing overlapping responsibilities, shifting family needs, and emotional decisions that cannot be solved by a spreadsheet alone.

Why This Pressure Builds Even When You’re Trying to Be Responsible

This problem usually does not come from one bad decision. It develops from a mix of family structure, economic pressure, emotional responsibility, and unclear boundaries over time.

One major reason it exists is that family systems tend to absorb stress by leaning on the most reliable person. In many families, there is one sibling, one adult child, one parent, or one couple who becomes the “financial shock absorber.” They step in during emergencies. They fill gaps. They keep things moving. Because they are competent and caring, more responsibility naturally starts flowing toward them.

Another reason is that different generations often face real financial strain at the same time. Children may need more support longer than expected because housing, education, childcare, and early adulthood are expensive. Parents may need more support as healthcare costs rise, retirement savings fall short, or independence becomes harder to maintain. That means the middle generation is not imagining the pressure. The pressure is often real on both sides.

There is also a timing problem. The years when adults are supposed to strengthen retirement savings, reduce debt, and build long-term security often overlap with the years when family support needs intensify. So even when someone is trying to be responsible, the structure around them keeps pulling resources into the present.

That helps explain an important truth: effort alone often does not solve this problem.

Many people assume that if they budget harder, work more, or become more disciplined, the situation will stabilize. Sometimes those things help at the margins. But multi-generational financial stress often persists because the issue is not just effort. The issue is competing obligations inside a system with limited capacity.

You can be hardworking and still overwhelmed if too many people depend on your stability.

You can be generous and still unsustainably stretched.

You can be organized and still feel like your long-term plans keep getting pushed further away.

A clarifying insight that often helps is this: the problem is not simply that you care too much or plan too little. The problem is that you may be trying to solve a multi-household stability issue with a one-household financial model.

That shift matters. It reframes the stress from personal failure to structural overload. It does not remove responsibility, but it does explain why the problem feels so persistent. You may not be dealing with a lack of willpower. You may be dealing with a financial role that has quietly become bigger than your current system can safely hold.

For people who want a deeper next step, structured support can help translate this kind of pressure into clearer priorities, steadier limits, and a more sustainable plan. That is the purpose behind A Multi-Generational Financial Stability Framework, which explores the issue in more depth without pressure or urgency.

Beliefs That Feel Responsible but Quietly Make the Stress Harder

When people are stuck in this kind of stress, it is often not because they do not care. It is usually because they are operating from beliefs that feel loving, responsible, or necessary in the moment, but quietly make the pressure harder to manage.

When Love Starts Getting Confused With Always Saying Yes

This belief is understandable because support and love are often deeply linked in family life. Many people were raised to believe that helping is what good family members do. The problem is that unlimited financial availability is not the same thing as love. When every request becomes an automatic yes, the most stable person in the system can become increasingly unstable too.

Over time, this can create resentment, depletion, and hidden fear. It can also prevent the family from having more honest conversations about what is sustainable.

When a Temporary Stretch Quietly Becomes the New Normal

Sometimes it is temporary. But in many families, support patterns become long-term without anyone formally deciding that they will. A few months of help becomes a year. A short-term gap becomes a standing expectation. An occasional emergency becomes an ongoing role.

This misconception is understandable because most people want to believe the pressure will ease soon. But if support has become recurring, it needs to be understood as a structure, not just an interruption.

Why Earning More Does Not Always Solve the Real Problem

More income can absolutely help. But income alone does not solve unclear expectations, repeated rescue patterns, or the absence of decision rules. Many people increase their earnings only to find that the emotional and financial demands rise with them.

This belief is understandable because earning more feels productive and concrete. But without structure, extra capacity often gets absorbed just as quickly as it appears.

Why Capable People Often Carry Too Much in Silence

A lot of capable adults believe they should be able to carry family pressure without needing to rethink the system. They may feel embarrassed that the situation is affecting them emotionally. They may minimize the stress because other people have it worse.

This is understandable too. Competent people often become the person everyone relies on, and that identity can make it difficult to admit that the load is too heavy. But staying silent does not make the strain less real. It usually just pushes the cost inward.

Why Setting Limits Is Not the Same as Letting People Down

This may be the most painful misconception of all. People often fear that any financial boundary will be interpreted as selfishness, betrayal, or lack of care. So they avoid limits entirely.

That response makes sense emotionally. But limits are not always rejection. Often, they are the thing that keeps support honest, stable, and possible. Without limits, support can become chaotic, unclear, and damaging to everyone involved.

The deeper issue beneath these misconceptions is that many people are trying to be both compassionate and endlessly available. Those are not the same thing. Compassion can be steady. Endless availability usually cannot.

What More Sustainable Support Starts to Look Like

The solution to multi-generational financial stress is usually not a single trick, a stricter budget, or one difficult conversation. At a high level, the path forward is about moving from reactive support to structured support.

That shift begins with a few key thinking changes.

1. See the Full Pattern, Not Just the Latest Request

When support needs are viewed one request at a time, every decision feels emotionally charged and urgent. But when the full pattern becomes visible, it is easier to understand what is actually happening. You are not just helping here and there. You may be functioning as part of a larger family stability system.

Seeing the pattern clearly reduces confusion. It helps you stop judging each moment in isolation and start recognizing the broader financial role you have taken on.

2. Separate Being Responsible From Carrying Everything

Many people confuse being responsible with absorbing every consequence. But those are different things. Responsibility can include care, contribution, communication, and planning. It does not have to mean protecting every person from every financial discomfort at all times.

This is a meaningful reframe. It allows support to become more deliberate instead of automatic. It creates room for the question: what is actually mine to carry, and what am I carrying because no one has named a limit yet?

3. Make Room for Today’s Needs Without Sacrificing Tomorrow

One of the hardest parts of this issue is that immediate needs feel morally louder than future needs. A parent’s bill due now or a child’s need today can feel more urgent than retirement savings, debt reduction, or long-term financial resilience.

But long-term stability matters precisely because family pressure is ongoing. If your own financial base keeps weakening, your ability to support anyone becomes more fragile. Sustainable support requires holding both timelines at once: the present and the future.

4. Stop Letting Guilt Make Every Financial Decision

When decisions are made mainly to reduce guilt, they tend to be inconsistent and exhausting. You may overgive one month, pull back sharply the next, then feel bad and overcorrect again. That pattern creates emotional volatility and weakens trust in your own judgment.

A stronger structure comes from principles. Principles create steadier decision-making. They do not eliminate emotion, but they prevent emotion from being the only thing steering the process.

5. Treat Clear Expectations as Part of Caring Well

Many families avoid clarity because they fear conflict, disappointment, or sadness. But vagueness often increases stress for everyone. It creates assumptions, silent pressure, and recurring confusion.

Clarity can feel uncomfortable at first, yet it often becomes one of the most respectful things a family can build. Clear expectations reduce panic. Clear limits reduce resentment. Clear roles make support easier to understand and maintain.

At the highest level, the real solution is not becoming harder or colder. It is becoming more structured, more honest, and more sustainable.

When Clearer Structure Starts to Feel Helpful

For some readers, understanding the problem clearly is already a relief. It helps explain why this stress has felt so persistent and personal.

For others, insight is only the first step. Once you can see the pattern, you may want more structure for how to think through competing responsibilities without falling into guilt, confusion, or constant reaction. That is where deeper guidance can be useful. Not because you need pressure, but because complex family financial roles often benefit from a calmer framework than scattered advice can provide.

A Clearer Way to Understand the Weight You’ve Been Carrying

Supporting multiple generations creates unique financial stress because the issue is not just money. It is money combined with care, identity, loyalty, timing, and the quiet weight of being the person others depend on.

That is why the problem can persist even when you are trying hard, planning carefully, and acting with good intentions. The strain often comes from structural overload, not personal failure. You may be carrying responsibilities that span multiple households, multiple timelines, and multiple emotional roles at once.

The most helpful shift is often recognizing that this is not simply a budgeting problem. It is a support-structure problem. And support becomes more sustainable when it is shaped by clarity, limits, and a longer view of stability.

You do not have to solve everything at once. But seeing the problem more accurately can reduce shame, soften confusion, and create calmer forward movement from here.

Download Our Free E-book!